Should I Invest a Lump Sum Right Away or Split It Into Multiple Amounts?

If you have your emergency fund set aside and have cash to invest, statistical probability based on a historical path shows that investing it right away is the best approach. It’s all about Time in the market not timing the market.

We are Sarwa

A one-stop shop for self-directed trading and auto-investing. We're making powerful money management tools available for all. Learn more.

May 12, 2020

Some investors are wondering if it is best to wait until the ‘uncertainty’ passes to invest their lump sum of cash.

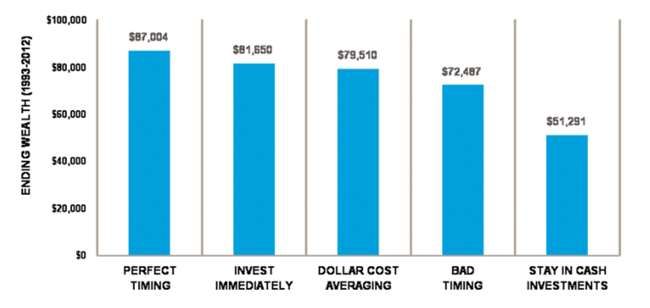

The reality is even bad timing in investing pays off more than not being in the market. This has been confirmed by many studies. Charles Schwab looked into the performance of five hypothetical long-term investors following very different investment strategies between 1993 and 2012.

The first makes annual deposits into their investment account and manages to perfectly time their deposit by investing at the market low for that year. The second always invests in January. Surprisingly, the study shows that there is little difference in portfolio performance for these two investors. The investor who successfully market times would earn less than 0.325% per year in extra returns compared to the investor who simply put her money to work as soon as she received it without even trying to time the market. The high probability of not getting the perfect timing, and loosing are not worth the incremental small returns.

However, the worst scenario is for the investor who decided to sit aside and staying in cash. While waiting for a better opportunity, he ended up losing the most.

As emotional investors, most of us would think that they should wait to see if it’s safe to go back in. However, waiting for everything to be back to normal to go in and expecting that this will have the best impact on returns simply does not work.

Source: Charles Schwab Study. Hypothetical $2000 annual investments in S&P 500 Index. Past performance is no guarantee of future results. The examples are provided for illustrative purposes only. Investors may not achieve similar results. The example does not reflect the effects of fees, taxes and potential costs.

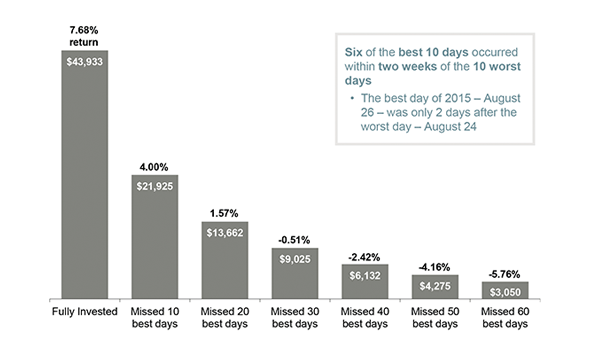

What happens if you miss the top 1 trading day each year?

JP Morgan ran a 20 years study of index annualized total returns of the S&P 500 between 1996 and 2015. what it showed is that trying to time that perfect day can be very costly.

Over the past 20 years the S&P 500 returned around 7.7% — with compounding interest this means your money would double every 9 years. That said, if you try to time the market and miss some of the best days in the market, these are what your returns would look like: 4.5% — if you miss the 10 best days in the past 20 years. 2% — if you miss the 20 best days. And if you miss the 30 best days you end up losing money.

Just recently, between March 23 and March 26 this year, and just in the matter of 3 days, the market increased by 19% – anyone who was not already in the market would have missed out on a substantial rebound.

Source: J.P. Morgan Asset Management analysis using data from Bloomberg. Returns are based on an unmanaged S&P Total Return Index. Past performance is no guarantee of future results. The examples are provided for illustrative purposes only. Investors may not achieve similar results.

Should you invest a lump sum right away or split it into multiple amounts?

If you have your emergency fund set aside and have cash to invest, statistical probability based on a historical path shows that investing it right away is the best approach. It’s all about Time in the market not timing the market.

If however you think the emotional rollercoaster is too much for you to handle, then you can split it in smaller sums. this is where Dollar Cost Averaging can benefit you. It prevents procrastination, and allows you to not have any regrets about not being in the market.

In summary,

Investing is not complicated. Working towards your long term goal is more important than short-term performance. One of the most important rule to get there is to control your emotions, stay the course and make sure your portfolio is rebalanced to stay aligned with your initial risk profile.

The information provided in this blog is for general informational purposes only. It should not be considered as personalised investment advice. Each investor should do their due diligence before making any decision that may impact their financial situation and should have an investment strategy that reflects their risk profile and goals. The examples provided are for illustrative purposes. Past performance does not guarantee future results. Data shared from third parties is obtained from what are considered reliable sources; however, it cannot be guaranteed. Any articles, daily news, analysis, and/or other information contained in the blog should not be relied upon for investment purposes. The content provided is neither an offer to sell nor purchase any security. Opinions, news, research, analysis, prices, or other information contained on our Blog Services, or emailed to you, are provided as general market commentary. Sarwa does not warrant that the information is accurate, reliable or complete. Any third-party information provided does not reflect the views of Sarwa. Sarwa shall not be liable for any losses arising directly or indirectly from misuse of information. Each decision as to whether a self-directed investment is appropriate or proper is an independent decision by the reader. All investing is subject to risk, including the possible loss of the money invested.